8) Loans Activity |

|

Objective: Calculate various loan options to consider the cost of borrowing.

About Loans

A Loan is money that you borrow and must repay.

Being able to borrow money allows you to have things before you can afford to pay for them. You may take out a Loan to purchase a home – this type of Loan is called a Mortgage. Then you live there while you repay the debt. You might take a Loan out to buy a car, and repay the Loan while you are driving the car.

Having the ability to borrow can improve your lifestyle and provide greater comfort than you might be able to otherwise afford. Without the ability to borrow, you would only be able to buy things by paying the full purchase price up front with cash.

The Loan Principal is the amount of money you borrow. The Loan Principal is usually repaid in one payment or several smaller payments. This is the Payment Period. Common Payment Periods are weekly, biweekly, and monthly. The total amount of time it takes to fully repay the Loan is called the Amortization Period.

Example: A Loan paid monthly for 12 months has an Amortization Period of 1 year. The amount of each of the 12 payments and the dates on which they are due are set out in an Amortization Schedule.

Loan repayment normally includes an additional amount, called Interest. The lender who gives the Loan risks losing money if the Loan is not fully repaid. Interest is a fee paid to the lender for taking this risk.

Interest is usually calculated as a percentage of the Loan Principal.

Example: Loan Principal is $100 and Interest Rate is 5% means that $5 of Interest will be paid by the borrower, for a total Loan repayment of $100 + $5 = $105.

The frequency in which Interest is calculated is the Compounding Period, and results in more Interest being charged the longer the Loan is unpaid. The more frequently the Interest is calculated (compounded), the higher the Interest costs will be. Concepts of Simple Interest versus Compounding Interest can be somewhat complicated but are worth spending time to learn.

The Interest Rate charged on a Loan will vary based on the Lender, the type of Loan, duration of Loan, and your credit history. If you have not been reliably repaying your debts, then you will have a poor credit history. A poor credit history may cause the Lender to worry about your ability to repay a Loan, and may result in the Lender charging a higher Interest Rate for this increased risk of loaning money to you.

When you consider the cost of borrowing money, you should consider the Interest you will have to pay.

A Loan is money that you borrow and must repay.

Being able to borrow money allows you to have things before you can afford to pay for them. You may take out a Loan to purchase a home – this type of Loan is called a Mortgage. Then you live there while you repay the debt. You might take a Loan out to buy a car, and repay the Loan while you are driving the car.

Having the ability to borrow can improve your lifestyle and provide greater comfort than you might be able to otherwise afford. Without the ability to borrow, you would only be able to buy things by paying the full purchase price up front with cash.

The Loan Principal is the amount of money you borrow. The Loan Principal is usually repaid in one payment or several smaller payments. This is the Payment Period. Common Payment Periods are weekly, biweekly, and monthly. The total amount of time it takes to fully repay the Loan is called the Amortization Period.

Example: A Loan paid monthly for 12 months has an Amortization Period of 1 year. The amount of each of the 12 payments and the dates on which they are due are set out in an Amortization Schedule.

Loan repayment normally includes an additional amount, called Interest. The lender who gives the Loan risks losing money if the Loan is not fully repaid. Interest is a fee paid to the lender for taking this risk.

Interest is usually calculated as a percentage of the Loan Principal.

Example: Loan Principal is $100 and Interest Rate is 5% means that $5 of Interest will be paid by the borrower, for a total Loan repayment of $100 + $5 = $105.

The frequency in which Interest is calculated is the Compounding Period, and results in more Interest being charged the longer the Loan is unpaid. The more frequently the Interest is calculated (compounded), the higher the Interest costs will be. Concepts of Simple Interest versus Compounding Interest can be somewhat complicated but are worth spending time to learn.

The Interest Rate charged on a Loan will vary based on the Lender, the type of Loan, duration of Loan, and your credit history. If you have not been reliably repaying your debts, then you will have a poor credit history. A poor credit history may cause the Lender to worry about your ability to repay a Loan, and may result in the Lender charging a higher Interest Rate for this increased risk of loaning money to you.

When you consider the cost of borrowing money, you should consider the Interest you will have to pay.

Terms to Know

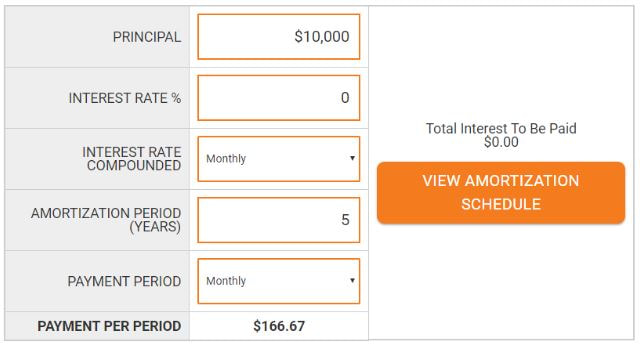

PRINCIPAL

The amount of money you want to borrow.

INTEREST

The extra fee you will pay in addition to the PRINCIPAL. INTEREST RATE is a percentage of the PRINCIPAL.

INTEREST RATE COMPOUNDED

How often Interest is calculated on the Loan – the Compounding Period.

AMORTIZATION PERIOD

The duration of the repayment.

PAYMENT PERIOD

The frequency in which you will make payments.

AMORTIZATION SCHEDULE

The amounts and dates due for each Loan payment.

How to Play

PRINCIPAL

The amount of money you want to borrow.

INTEREST

The extra fee you will pay in addition to the PRINCIPAL. INTEREST RATE is a percentage of the PRINCIPAL.

INTEREST RATE COMPOUNDED

How often Interest is calculated on the Loan – the Compounding Period.

AMORTIZATION PERIOD

The duration of the repayment.

PAYMENT PERIOD

The frequency in which you will make payments.

AMORTIZATION SCHEDULE

The amounts and dates due for each Loan payment.

How to Play

- Enter values for each item.

- Review the PAYMENT PER PERIOD and TOTAL INTEREST TO BE PAID. Experiment with the numbers to see how they change.

- Use the PRINT button to print to paper or save as an electronic file (pdf). Write your name down on the printout if you will be submitting to an instructor.

- Use the RESET button to erase your data or start over.

|

PRACTICE

Click the PLAY ACTIVITY button below to do the activity for MO and then for yourself. Mo Money Play this activity to determine the biweekly car payment and monthly loan (mortgage) payment for Mo Money, based on his future loans. Review the MO MONEY PROFILE. YOUR TURN! Complete your own LOANS activity. |