4) Budget & Cash Flow Activity |

BACK to ACTIVITIES PAGE |

|

Objective: Play this activity to add up all the money you receive each month and subtract all the money you pay out.

About Budget & Cash Flow

Cash Flow

Making money and spending money represent the basic concept of Cash Flow — how money flows in and out of your accounts: Money in minus money out.

Cash Flow

Making money and spending money represent the basic concept of Cash Flow — how money flows in and out of your accounts: Money in minus money out.

Cash Flow = Money IN – Money OUT

Money IN

Making money represents all the ways you receive money. You might make money by working at a job, by buying and selling stocks, earning an allowance, or even winning the lottery. These are your sources of incoming cash and are called Income – this is your Money IN.

Money OUT

Spending money is something that most people find easy to do. Spending represents the uses of your money. Your current expenses cover the essential cost of living — expenses such as housing, transportation, food, and clothing.

Additional discretionary expenses include entertainment, extra clothes, hobbies, education, and charitable donations. Discretionary expenses are those expenses over which you have more control, and which are not mandatory for you to live and earn your wages.

Money you spend for living and discretionary purchases are Money OUT.

Money OUT also includes money you set aside for saving, an emergency fund, etc. Your not spending this money, so it is not considered an expense. But, it is recorded as Money OUT because it affects your Budget and Cash Flow, as it is money that you have chosen not to make available for other purposes.

Period

The PERIOD is the duration of time in which you are tracking your Money IN and Money OUT. Often, this is monthly, but could be weekly, quarterly, yearly, or other time period. For example, with a monthly time PERIOD, you list your Money IN and Money OUT during that particular month.

NOTE: When converting a weekly amount to a monthly amount, multiply by 4. When converting a monthly amount to weekly, divide by 4. This is not exact, but makes it simple. The more exact multiplier or divisor is actually 4.334.

Calculating your Money IN minus Money OUT tells you if you will have enough money available to pay your bills and set aside for saving.

Surplus – you have more Money IN than OUT. That’s good! Having a surplus is also called being “in the black”, which refers to the ink color bookkeepers historically used to mark down positive numbers.

Deficit – you have more Money OUT than IN. Not so good! You have to reduce what you are spending money on, or reduce savings, or find a way to make or borrow more money. Having a deficit is also called being “in the red”, which refers to the ink color bookkeepers historically used to mark down negative numbers.

Budget

A Budget is an itemized list of estimated expenditures and the expected ways to pay for them, for a given time period. By budgeting you can manage your finances better, and watch to make sure you don’t spend more money than you budgeted.

In addition to income and expense items, Budgets often include planned amounts for savings or investment. For example, you might have money taken out of your pay cheque for a retirement plan. Or, you might make monthly payments to a savings account or emergency fund. These are uses of your cash that may remove it from easy access, but the money is still yours. Think of it as paying yourself.

Budget Versus Cash Flow

The main difference between a Budget and a Cash Flow is that a Budget uses estimates and a Cash Flow uses actual amounts. A Budget is an estimate, done before the money is earned and spent or set aside. A Cash Flow shows actual results of earnings, expenses, and money set aside. It is also useful to compare your Budget with what actually happened. This helps you to make your future Budgets more accurate.

How to Play

Making money represents all the ways you receive money. You might make money by working at a job, by buying and selling stocks, earning an allowance, or even winning the lottery. These are your sources of incoming cash and are called Income – this is your Money IN.

Money OUT

Spending money is something that most people find easy to do. Spending represents the uses of your money. Your current expenses cover the essential cost of living — expenses such as housing, transportation, food, and clothing.

Additional discretionary expenses include entertainment, extra clothes, hobbies, education, and charitable donations. Discretionary expenses are those expenses over which you have more control, and which are not mandatory for you to live and earn your wages.

Money you spend for living and discretionary purchases are Money OUT.

Money OUT also includes money you set aside for saving, an emergency fund, etc. Your not spending this money, so it is not considered an expense. But, it is recorded as Money OUT because it affects your Budget and Cash Flow, as it is money that you have chosen not to make available for other purposes.

Period

The PERIOD is the duration of time in which you are tracking your Money IN and Money OUT. Often, this is monthly, but could be weekly, quarterly, yearly, or other time period. For example, with a monthly time PERIOD, you list your Money IN and Money OUT during that particular month.

NOTE: When converting a weekly amount to a monthly amount, multiply by 4. When converting a monthly amount to weekly, divide by 4. This is not exact, but makes it simple. The more exact multiplier or divisor is actually 4.334.

Calculating your Money IN minus Money OUT tells you if you will have enough money available to pay your bills and set aside for saving.

Surplus – you have more Money IN than OUT. That’s good! Having a surplus is also called being “in the black”, which refers to the ink color bookkeepers historically used to mark down positive numbers.

Deficit – you have more Money OUT than IN. Not so good! You have to reduce what you are spending money on, or reduce savings, or find a way to make or borrow more money. Having a deficit is also called being “in the red”, which refers to the ink color bookkeepers historically used to mark down negative numbers.

Budget

A Budget is an itemized list of estimated expenditures and the expected ways to pay for them, for a given time period. By budgeting you can manage your finances better, and watch to make sure you don’t spend more money than you budgeted.

In addition to income and expense items, Budgets often include planned amounts for savings or investment. For example, you might have money taken out of your pay cheque for a retirement plan. Or, you might make monthly payments to a savings account or emergency fund. These are uses of your cash that may remove it from easy access, but the money is still yours. Think of it as paying yourself.

Budget Versus Cash Flow

The main difference between a Budget and a Cash Flow is that a Budget uses estimates and a Cash Flow uses actual amounts. A Budget is an estimate, done before the money is earned and spent or set aside. A Cash Flow shows actual results of earnings, expenses, and money set aside. It is also useful to compare your Budget with what actually happened. This helps you to make your future Budgets more accurate.

How to Play

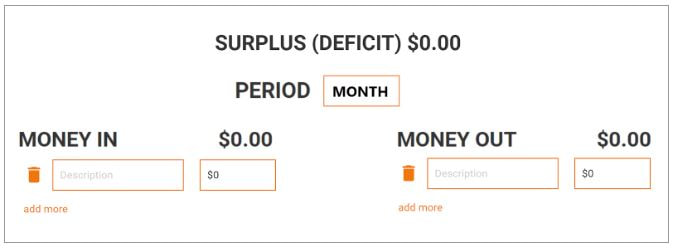

- Choose a PERIOD.

- Under MONEY IN, click ADD MORE and enter the description and amount of an item you want to add. The amount should be the estimated or actual amount received during the set PERIOD. Repeat this step to add all MONEY IN. Click the trash can to remove an item.

- Under MONEY OUT, click ADD MORE and enter the description and amount of an item you want to add. The amount should be the estimated or actual amount received during the set PERIOD. Repeat this step to add all MONEY OUT. Click the trash can to remove an item.

- CASH FLOW is automatically calculated based on MONEY IN minus MONEY OUT. If you change the PERIOD after you enter MONEY IN or OUT items, they will be recalculated based on the new PERIOD.

- Use the PRINT button to print to paper or save as an electronic file (pdf). Write your name down on the printout if you will be submitting to an instructor.

- Use the RESET button to erase your data or start over.

|

PRACTICE

Click the PLAY ACTIVITY button below to do the activity for MO and then for yourself. Mo Money Play this activity to determine the Budget & Cash Flow for Mo Money, based on his current income and expenses. When calculating monthly amounts, multiply weekly amounts by four (this is not quite exact, but keeps it simple). Review the MO MONEY PROFILE. YOUR TURN! Complete your own Budget & Cash Flow. |